Working capital is a fundamental component of any thriving business.

One of the most important aspects of procurement is understanding and utilizing working capital in the best way possible to ensure you are making the most of your resources.

Let’s dig into what working capital is, how it can be calculated, and why it’s important.

What is Working Capital?

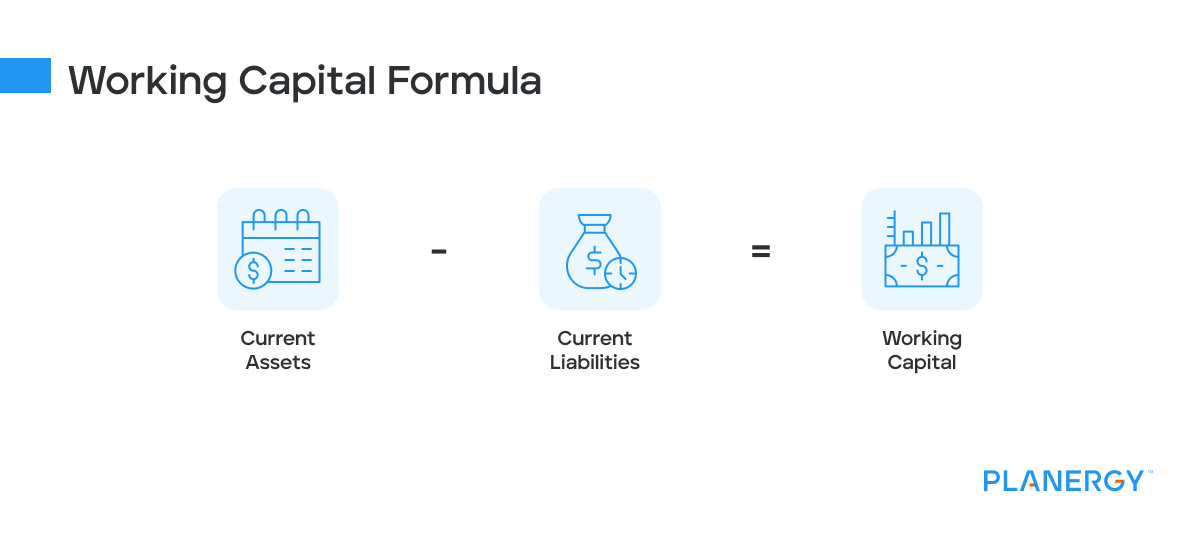

Working capital, sometimes referred to as net working capital, is a company’s current assets minus its current liabilities.

Assets are items a company owns that can be sold or converted into cash quickly; these include inventory, accounts receivable, and short-term investments.

Liabilities are obligations that must be paid off within one year; they include accounts payable, taxes payable, and short-term debt.

Working Capital Example

For example, if a company has $2 million in cash on hand (current asset) and $1 million in accounts payable (current liability), then its amount of working capital would be $1 million ($2 million – $1 million).

Working capital measures how efficiently a business uses its resources to generate sales and profits. In other words, it indicates how well the company manages its short-term financial obligations.

Positive working capital indicates that a company has enough liquid assets (cash flow) to cover its current debts.

In contrast, negative working capital suggests it may not have enough liquid assets to cover its current liabilities. It’s an important metric to monitor your company’s financial health.

How to Calculate Working Capital

The net working capital formula is:

Current assets – Current liabilities = working capital

To calculate working capital, you’ll need the balance sheet.

Add up the values of your company’s current assets (cash on hand and cash equivalents, accounts receivable, inventory, etc.).

Subtract your total current liabilities (accounts payable, short-term debt payments due within one year).

The resulting number will be your working capital. Remember that this number should always be positive; if it isn’t, you may need to adjust your budget or restructure some of your debt payments to ensure adequate business liquidity.

Current Assets

This includes cash and liquid assets that can be converted to cash within 12 months of the balance sheet, such as:

- Cash – money in bank accounts and any deposited customer checks

- Marketable securities – money market funds, U.S. treasury bills, etc.

- Prepaid expenses – rent, insurance premiums, utilities, etc.

- Short-term investments the company plans to sell within 12 months.

- Inventory – raw materials, finished goods, and works in progress

- Accounts receivable, minus allowances for any payments expected to be written off as bad debts.

- Notes receivable – short term loans to suppliers or customers that will mature within 12 months

- Any other receivables – cash advances to employees, tax refunds, insurance claims, etc.

Current Liabilities

This refers to any liability due within 12 months of the balance sheet, including:

- Loan principle that must be paid within a year

- Deferred revenue – advanced payment from customers for goods or services not yet rendered

- Wages payable

- Taxes payable

- Accounts payable

- Notes payable due within 12 months

- Interest payable on any loans

- Any other accrued expenses payable

Why Working Capital is Important to Your Organization

Regardless of industry, chances are you have some seasonal fluctuations in revenue.

The hospitality industry, for instance, tends to earn more in the summer when everyone’s on vacation. Retailers tend to earn more toward the end of the year when everyone is focused on holiday shopping.

However, those businesses have to cover expenses, such as rent/mortgage, payroll, and utilities year-round.

With adequate spend forecasting and working capital management, those businesses can make sure they have enough cash to build a supply stock before the busy season and hire temporary employees while also ensuring they can support the permanent staff.

What is a Good Working Capital Ratio?

The working capital ratio, also known as working capital ratio, is your current assets divided by your current liabilities.

If your ratio is less than one – the business isn’t generating the revenue it needs to meet the company’s short-term obligations.

If the ratio falls between 1.2 and 2.0, your company is using its assets well.

A ratio of 2.0 or higher indicates maintenance of a lot of short-term assets, and the money could be put to better use by reinvesting the funds to generate more revenue.

In the example above, $2 million in assets and $1 million in liabilities creates a ratio of 2.0, so the volume of short-term assets hampers the company’s ability to generate revenue.

As an alternative to the current ratio, you can also use the quick ratio, which only includes the company’s most liquid assets – the ones that have a short cash conversion cycle.

Improving your working capital ratio means taking action to improve cash flow.

Tips for Improving Working Capital

If you find your company needs to improve working capital, there are several things you can do.

Avoid Financing Fixed Assets with Working Capital

Fixed assets cannot be easily converted to cash, so they’re not included in the current assets. This means you should avoid using your working capital to finance equipment, facilities, real estate, trademarks, and patents.

Selling fixed assets can boost your working capital and cash flow, but financing them with working capital isn’t smart because they tend to be expensive.

It depletes working capital reserves and increases your risk profile with lenders and other credits. You’re better off using long-term liabilities to address these needs.

Run Credit Checks on New Customers

Researching a new client’s or prospect’s creditworthiness is essential to determine if they are a sound candidate for extending credit. Credit reports can offer valuable insight, aiding you in understanding their payment history and public records.

However, as this data can become obsolete quickly, you must also consider the industry in which the company operates and any local market nuances that could be of significance before approving them for credit.

By considering all of this, you can make an educated decision about whether or not offering a line of credit is worthwhile and appropriate.

Reduce Risk of Bad Debt

Bad debt can quickly snowball and erode a company’s working capital, leaving it with limited resources to meet current financial commitments.

Businesses looking to reduce the impact of such debt need to be proactive in tackling the issue – by selling higher-margin products or increasing their margins across offerings, introducing tighter credit management processes, speeding up payment collections, and utilizing just-in-time logistics to recalibrate stock levels.

Although this may require an investment of time and resources upfront, protecting your business from expensive losses will pay off in the long run.

Improve Cash Flow Cycle Time

Increasing cash flow is a key component for driving working capital, and there are multiple ways to turn money tied up in the production or sales cycle into cash.

Options worth exploring include: asking for upfront payments on orders, reducing credit terms, billing customers immediately upon sale, or getting a better grip on sales forecasting/demand planning.

It’s important to accurately understand what demand is likely to be to ensure that you can properly manage cash flow while accommodating customer needs.

Flexibility in your operating cycle is necessary to remain competitive and make the most of your working capital. It is especially important to manage working capital well when you are experiencing an increase in business operations.

Seek Additional Long-Term Bank Financing

You can add to the company’s available cash by taking on more long-term debt without overly increasing your short-term liabilities.

You may also wish to consider refinancing some short-term debts into long-term ones. Since the debts are no longer due within 12 months, you’ll decrease your current liabilities.

Reduce Unnecessary Spend and Expenses

Regularly analyze your business expenses, especially the variable ones. With analysis, you can gain insight into how you may be able to restructure your costs and pricing to increase working capital or cut overall costs.

You can accomplish this by negotiating discounts with the most important suppliers in your supply chain, or finding suppliers who offer better pricing.

Regular analysis also helps you find other cost savings opportunities without sacrificing product or service quality.

Invest in Trade Credit Insurance

Trade credit insurance is a valuable tool for businesses seeking to protect their capital from late or non-existent payments. It acts as a financial safety net by insuring accounts receivable and helping to offset the costs of bad debt reserves.

Not only that, banks recognize this insurance and may offer businesses lower interest rates on loans because their accounts receivable are secured collateral.

Trade credit insurance provides the security of protection while freeing up capital in the long run and allowing companies to expand growth opportunities.

Optimize Inventory Management

You’ll spend less overall by reducing overstock and the chance that you’ll have to write off bad inventory. This frees up revenue to reinvest in other areas of the business. Good inventory management processes can help improve cash flow.

Working Capital Management

This is managing managing a company’s current assets and liabilities to ensure adequate liquidity to meet its short-term obligations and remain profitable over time.

Proper management allows your business to maintain sufficient liquidity to cover its short-term debt obligations without taking on additional debt or selling off assets.

This helps you remain competitive in the marketplace while also preserving your ability to take advantage of potential opportunities that may arise in the future.

By keeping an eye on current assets and liabilities, businesses can better anticipate potential cash flow problems before they become critical issues.

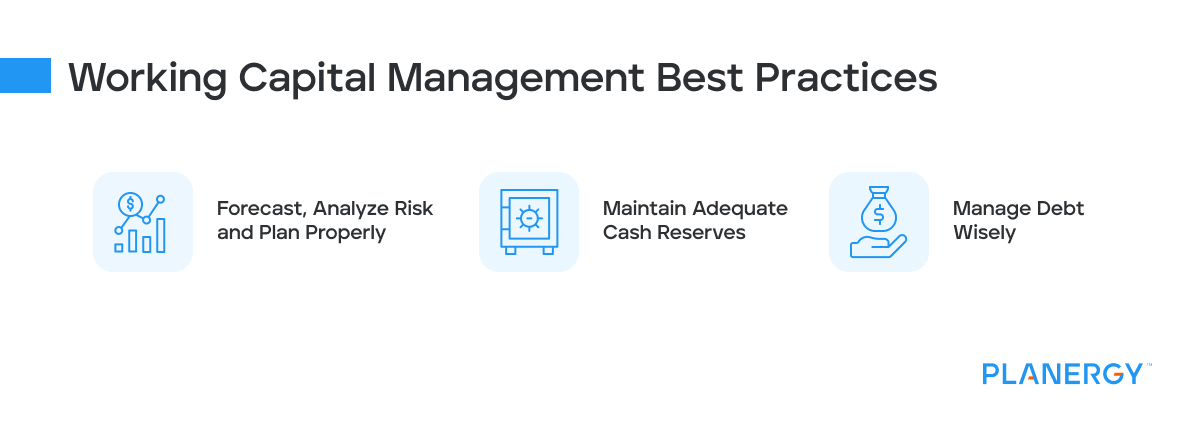

Forecast, Analyze Risk and Plan Properly

This includes forecasting cash flow needs, setting aside necessary funds for future investments, and creating a budget with realistic goals and objectives.

Having a plan will help you anticipate potential problems before they arise and identify areas where your business can make cost savings or increase revenues.

It will also give you an idea of how much money you need to keep on hand for contingencies or unexpected expenses.

Maintain Adequate Cash Reserves

It’s important to maintain adequate cash reserves to ensure that your business always has access to the funds it needs when it needs them.

This means setting aside enough monthly money so your business can weather any unexpected expenses or slow periods without having to borrow from outside sources or dip into other accounts.

You should also consider investing in short-term investments like CDs or Treasury bills to grow your cash reserves while taking advantage of higher interest rates than traditional savings accounts offer.

Manage Debt Wisely

Make sure you don’t take on too much debt at once and ensure that any loans are at reasonable interest rates with set repayment schedules that fit within your budget.

It also means avoiding high-risk investments or speculative ventures, as these can quickly strain your finances if things don’t pan out as expected. Pay off any existing debt as soon as possible so that more money is available for other endeavors.

Understanding and managing working capital is essential for any successful procurement professional who wishes to optimize their company’s resource utilization while maximizing profits.

Being mindful of liquidity enables you to make informed decisions about your purchases while negotiating better payment terms with suppliers when necessary.

By being aware of how much debt you can handle without compromising future operations or profits, you can help ensure the business remains afloat in any economic landscape—now more than ever!